Linking Entities to Expose and Disrupt Fraud Networks

For SIU and claims executives, organized fraud presents a fundamentally different challenge than opportunistic misconduct. It is not simply a matter of one inflated bill, one misrepresented injury, or one suspicious loss. Organized fraud is structured, repeatable, and designed to exploit gaps between claims handling, vendor oversight, and investigative workflows. What appears to be a single questionable claim is often part of a broader network involving false claimants, shell companies, staged incidents, recruited participants, and service providers working in coordination.

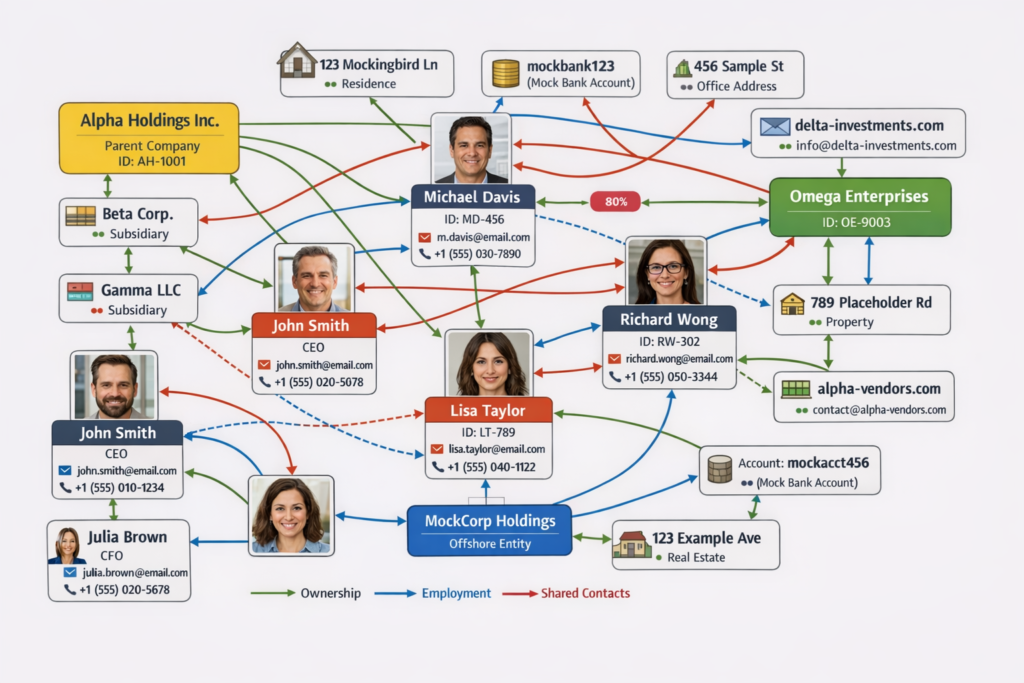

This distinction matters. When fraud is assessed only at the file level, insurers risk addressing the symptom rather than the operation behind it. Organized rings understand this. They rely on fragmentation across claims, business entities, geographies, and internal departments. Their advantage comes from appearing disconnected. The insurer’s advantage comes from doing the opposite: linking people, businesses, addresses, vehicles, digital identities, and prior claims into a single investigative picture.

That is why entity-based investigation has become a critical capability for modern SIU and claims leadership. Specialized social media investigations and open source intelligence can help insurers identify hidden relationships, validate patterns of coordination, and move from isolated suspicion to network-level disruption.

Why Organized Fraud Requires a Different Response

Traditional claims indicators remain important, but in organized fraud they are rarely enough on their own. A questionable treatment pattern, a recently incorporated vendor, or a claimant with limited documentation may all raise concerns, yet none necessarily proves coordinated fraud. What changes the equation is linkage.

A claimant may share an address, phone number, or online association with individuals in prior suspicious files. A repair facility may be tied through corporate records to other entities involved in similar claims. A medical provider, legal referral source, towing operator, and claimant may appear unrelated inside separate claim files, while public records and social media reveal repeated interaction and common control. Once those linkages are identified, the claim no longer stands alone. It becomes part of a pattern.

For SIU and claims executives, this is the shift that drives better outcomes. The objective is not only to determine whether one claim should be denied, defended, or escalated. It is to understand whether the insurer is dealing with a repeatable fraud model that will continue generating losses unless the broader network is identified and addressed.

The Role of Specialized Social Media and Open Source Investigations

Open source intelligence and social media investigations give insurers access to a broader layer of evidence that is often unavailable through the claim file alone. These methods rely on publicly available information drawn from corporate registries, court filings, property records, licensing data, archived websites, mapping tools, business listings, social platforms, and other lawful public sources.

For organized fraud investigations, their value lies in exposing relationships.

Corporate records may reveal that multiple vendors tied to suspicious claims share directors, officers, registration agents, mailing addresses, or contact details. Public databases may show that a claimant, witness, or business owner has appeared in prior litigation, prior losses, or other entities that raise concern. Social media may reveal that people presented as independent parties are in fact connected through family, social circles, business promotion, shared travel, or common affiliations.

These findings are rarely decisive in isolation. Their value comes from being combined. A shell company with no obvious operating footprint may seem merely unusual until it is linked to a claimant’s associate, a common address, and a referral pattern across multiple losses. A claimant’s online activity may not only undermine an injury narrative, but also connect them to another participant in a separate suspicious claim. Once those connections are mapped, the operational structure of the fraud ring becomes clearer.

Entity Linking as an Executive-Level Capability

Entity linking is more than an investigative technique; it is an enterprise fraud capability. It allows insurers to connect data points that would otherwise remain buried across claim files, policy systems, vendor records, and public sources. For claims and SIU leadership, this means transitioning from case-by-case review to intelligence-led fraud management.

The entities most often linked in organized fraud matters include:

-

Claimants and passengers

-

Witnesses and recruiters

-

Medical and legal referral sources

-

Repair shops, towing companies, and transportation vendors

-

Shell companies and related business entities

-

Addresses, phone numbers, email addresses, and websites

-

Vehicles, plates, and incident locations

-

Social media profiles and online associations

When these links are visualized and continuously updated, investigators can identify clusters, recurring combinations, and central actors in the network. This is especially important in organized fraud, where peripheral participants may change but infrastructure often remains stable. Addresses are reused. Companies are dissolved and recreated. The same service providers reappear. Digital contact points remain consistent. Social relationships persist even when business names change.

For executives, the implication is clear: the insurer that can detect recurring entities and relationships early will outperform the insurer that only reviews suspicious facts within one file at a time.

Corporate Records and Public Databases as Force Multipliers

Corporate records are especially valuable in exposing shell structures used to facilitate fraud. Organized rings often create or control businesses that appear legitimate enough to receive payments, generate invoices, or support a claim narrative. These entities may be presented as independent repair shops, transport companies, consulting firms, wellness providers, or administrative services. Public records can often show otherwise.

Patterns that matter include overlapping directors, recently formed corporations with immediate claims activity, multiple entities tied to a single registered address, repeated use of the same contact information, and businesses with minimal real-world presence. Public mapping and address verification can help determine whether a location is consistent with the operation claimed. Litigation and licensing records can provide additional context on credibility, operating history, and prior issues.

For SIU leaders, these are not merely investigative details. They are strategic data points that help determine whether a vendor, claimant cluster, or line of business warrants broader review. For claims executives, they support more confident escalation decisions, stronger litigation positioning, and more effective allocation of investigative resources.

Social Media Intelligence and Relationship Analysis

Social media is often where concealed relationships become visible. Organized fraud participants may separate their formal documentation, but they are less disciplined in managing digital association over time. Connections can surface through shared followers, tagged images, mutual comments, event attendance, business promotion, and repeated interactions across platforms.

In the SIU context, social media should not be viewed narrowly as a tool for catching one claimant in contradiction. Its greater value is in relationship analysis. A claimant may be linked online to a towing operator involved in prior suspicious losses. A business owner may interact regularly with multiple claimants, service providers, or recruiters. Profiles on different platforms may share usernames, contact details, or imagery that connect aliases and entities together.

This broader use of social media intelligence is particularly important for organized fraud because it helps answer the executive question that matters most: is this an isolated concern, or are we looking at a network?

Operational Benefits for SIU and Claims Leadership

A network-based approach to fraud investigation delivers practical benefits across the claims organization.

First, it improves early detection. When entities are linked across files, suspicious patterns can be identified sooner, often before losses escalate across multiple claims.

Second, it supports better triage. Not every suspicious claim warrants the same response. Entity analysis helps SIU and claims leaders distinguish between one-off concerns and high-risk networks with recurring exposure.

Third, it strengthens case strategy. Denials, coverage decisions, examinations under oath, litigation referrals, and regulatory referrals are more persuasive when supported by a clear pattern of linked activity rather than isolated anomalies.

Fourth, it enhances cross-functional alignment. Claims, SIU, legal, compliance, and vendor oversight teams are more effective when operating from a common intelligence picture of the entities involved.

Fifth, it drives long-term fraud reduction. When insurers identify the infrastructure of organized fraud — not just individual participants — they can flag related entities prospectively, monitor emerging patterns, and reduce repeat losses over time.

Moving from Claim Investigation to Network Disruption

The central objective for insurers should not be limited to resolving one suspect claim. It should be to identify and disrupt the broader fraud ecosystem generating those claims. That requires a shift in mindset from file review to network analysis.

For SIU and claims executives, this means investing in capabilities that support cross-file entity resolution, open source research, social media intelligence, and structured relationship mapping. It also means ensuring that investigative findings are not trapped within individual claim notes, but instead contribute to a cumulative intelligence model that can inform future detection, referral, and litigation strategy.

Organized fraud rings are built on repetition, coordination, and concealment. They succeed when insurers treat each event as independent. They become vulnerable when insurers connect the underlying people, companies, digital identities, and operational touchpoints that tie the scheme together.

In that sense, entity linking is not simply an investigative enhancement. It is a strategic defense against a category of fraud that is increasingly organized, increasingly adaptive, and increasingly costly. Insurers that combine specialized social media investigations with open source intelligence and entity-based analysis are better positioned to detect organized activity early, dismantle fraud networks more effectively, and protect both claim outcomes and enterprise performance.